Introduction

B2B commerce sits at the center of global trade. Yet despite representing a multi-trillion-dollar market, B2B retail payments remain surprisingly manual. Many retailers still rely on spreadsheets, email-based approvals and loosely enforced credit policies to manage transactions that can involve six- or seven-figure orders.

At the same time, expectations on the buyer’s side have changed dramatically. Corporate procurement teams now expect the same speed, transparency and flexibility they experience in consumer purchasing, even when transactions involve complex approval chains, negotiated pricing or regulatory requirements.

This mismatch has created a widening automation gap. Retailers are under pressure to scale B2B revenue, expand into new channels and geographies and improve customer experience — all without increasing finance headcount or taking on excessive risk.

According to Flagship Advisory Partners’ 2025 benchmark research, the retailers making the most progress are not those adopting isolated automation tools. They are the ones treating Pay by Invoice as foundational infrastructure for modern B2B buyer programs — a theme explored throughout the benchmark report, “Opportunities to Digitize B2B Commerce with Pay by Invoice and the Automation Flywheel”.

Unlock the full benchmark insights

Flagship’s analysis draws on benchmark data from enterprise retailers across the U.S. and EU, examining corporate buyer program performance across onboarding, credit decisioning, invoicing, payments and reconciliation.

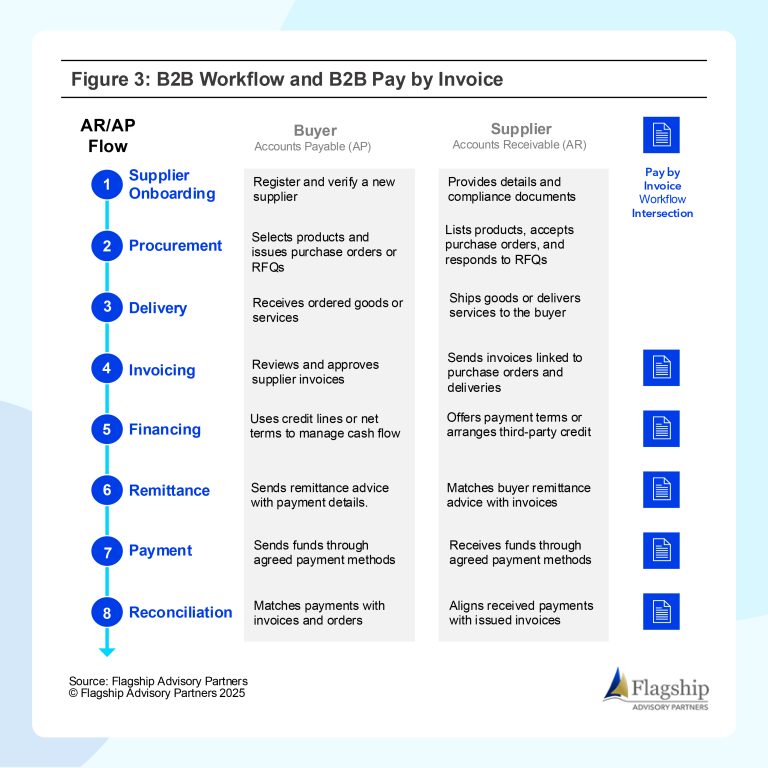

Importantly, Pay by Invoice is not just a payment mechanism. For leading retailers, it is the operational backbone of scalable corporate buyer programs. Formalizing Pay by Invoice requires retailers to define onboarding standards, credit policies, invoicing structures and settlement rules — the same building blocks required to support repeatable, cross-channel B2B buyer experiences at scale.

What the Benchmark Reveals About Corporate Buyer Programs

Flagship Advisory Partners’ study examined how leading retailers across the U.S. and EU structure B2B buyer programs, from onboarding and credit decisioning to invoicing, payment execution and reconciliation.

The research surfaces several important data points:

- Invoice automation is the top priority for A/R digitization initiatives among leading retailers (Opportunities to Digitize B2B Commerce with Pay by Invoice and the Automation Flywheel), underscoring how central structured invoicing has become to scalable B2B operations.

- Only 43% of NRF Top-30 retailers in the U.S. and 30% of NRF Top-20 retailers in the EU/U.K. currently enable corporate buyer portals (Opportunities to Digitize B2B Commerce with Pay by Invoice and the Automation Flywheel), revealing significant room for modernization in buyer-facing infrastructure.

- Among retailers that do offer corporate buyer portals, 95% support multiple payment methods (Opportunities to Digitize B2B Commerce with Pay by Invoice and the Automation Flywheel), demonstrating that mature programs prioritize flexibility and buyer choice.

These findings reveal a clear pattern: retailers with formalized Pay by Invoice programs consistently outperform peers across key financial and operational metrics, including:

- Higher average order values, driven by predictable purchasing power once buyers are approved

- Faster cash collection and more stable DSO, supported by standardized settlement schedules

- Lower cost to serve, as manual intervention and exception handling decline

- Stronger buyer loyalty, fueled by frictionless repeat purchasing and clear payment expectations

Importantly, these results don’t come from simply “offering net terms.” They come from embedding Pay by Invoice into the operating fabric of corporate buyer programs, making it a governed, scalable capability rather than an exception-based accommodation.

Why Pay by Invoice Is No Longer Only a Payment Option

Historically, Pay by Invoice was often extended informally, used to support trusted customers or accommodate large transactions. In many organizations, it still operates this way today: selectively offered, manually managed and reconciled after the fact.

At scale, this approach becomes a liability.

Today, Pay by Invoice must function as infrastructure in B2B retail. When treated as such, it becomes a unifying layer that connects credit decisioning, invoicing, payment execution and cash application, from authorization through settlement, into a single, governed process.

This shift matters because every downstream automation effort depends on it. Without standardized invoice formats, consistent credit decisioning and predictable settlement logic, automation tools struggle to deliver value.

Infrastructure first. Automation second.

Stop managing net terms. Start building infrastructure.

Benchmark research shows that retailers frequently overestimate the maturity of their A/R and A/P workflows. Fragmented onboarding, inconsistent invoicing and manual reconciliation often persist unnoticed until organizations apply a structured maturity assessment.

The Four Pillars Pay by Invoice Connects

When implemented deliberately, Pay by Invoice aligns four critical elements of the order-to-cash lifecycle — a core requirement for scalable automation:

- Credit and Risk Decisioning

Approvals move from ad-hoc judgment calls to structured, repeatable processes that scale across buyers and regions. - Invoice Creation and Compliance

Invoices are generated consistently, aligned with buyer requirements and regulatory standards, reducing disputes and delays. - Payment Execution

Buyers transact with confidence, knowing terms, amounts and timing are predictable across channels. - Reconciliation and Cash Application

Payments are matched quickly and accurately, improving visibility, forecasting and control.

Together, these pillars create the conditions needed for real automation.

The Automation Flywheel Starts with Structure

One of the most important insights from the benchmark report is how structured Pay by Invoice programs unlock an automation flywheel.

As transactions become standardized, retailers gain clean, consistent data. That data enables:

- Automated invoice delivery and validation

- Faster cash application

- Predictive collections workflows

- Smarter credit and risk management

- AI-driven insights across A/R and A/P

In contrast, retailers that delay formalization often layer automation tools on top of fragmented workflows, resulting in limited ROI and mounting operational complexity.

Pay by Invoice is not the end state. It is the on-ramp to scalable automation.

What Leading Retailers Are Doing Differently

Top-performing retailers don’t treat Pay by Invoice as an exception. They design corporate buyer programs intentionally, a hallmark of operational maturity in B2B retail.

Leading retailers build programs with:

- Defined onboarding and approval processes

- Consistent invoice formats across buyers and regions

- Embedded settlement schedules

- Clear ownership between sales, finance and operations

The result is a buyer experience that feels effortless and a finance operation that remains predictable even as volume grows.

These organizations aren’t just automating faster. They’re building systems that scale.

Why This Matters for CFOs and Operations Leaders

For CFOs, Pay by Invoice infrastructure delivers measurable financial control — and provides the foundation for a credible modernization of finance operations:

- Lower and more predictable DSO

- Improved cash forecasting

- Reduced working capital volatility

- Stronger auditability and compliance

For operations leaders, it removes friction from daily workflows:

- Fewer exceptions

- Less manual reconciliation

- Better visibility across channels

Most importantly, it enables growth without proportional increases in cost or risk.

Pay by Invoice is the core infrastructure for modern B2B retail. See how leading retailers are structuring their buyer programs.

FAQ

What is Pay by Invoice for B2B retailers?

Read Response

Pay by Invoice is a payment model that allows approved business buyers to purchase goods on net terms rather than paying upfront. For retailers, it becomes a structured way to manage corporate buyer programs across onboarding, credit approval, invoicing and settlement. When implemented intentionally, it connects these workflows into a governed order-to-cash process. This enables retailers to support large B2B transactions while maintaining financial control and operational consistency.

How is Pay by Invoice different from traditional trade credit?

Read Response

Traditional trade credit is often extended informally and managed through manual processes such as spreadsheets or email approvals. Pay by Invoice infrastructure formalizes those workflows by standardizing credit decisioning, invoicing logic and settlement terms across buyers and channels. The difference is governance and scalability. Instead of ad-hoc exceptions, retailers operate a repeatable system that supports automation and growth.

How does Pay by Invoice improve DSO and cash flow?

Read Response

Pay by Invoice improves DSO when credit decisioning, invoicing and settlement schedules are standardized and enforced consistently. Rather than relying on reactive collections, structured programs automate invoice delivery, clarify payment timing expectations, enable predictive collections workflows.

What are the key capabilities of a Pay by Invoice solution?

Read Response

A modern Pay by Invoice solution goes far beyond simply offering net terms. It should operate as structured infrastructure across the order-to-cash lifecycle. Core capabilities include: automated credit and risk decisioning; smart invoice generation and delivery; payment execution and settlement orchestration; automated cash application and reconciliation; integrated collections workflows; ERP and commerce system integrations.